Banks are shifting from conventional approaches to more tech-savvy and time-saving methods for transactions. These specific credentials enable the bank to process and monitor the transfers and make them safe and timely. IFSC code is one such important credential that you usually come across while using several banking procedures.

IFSC code is an important detail you would be prompted to fill in almost every time you make payments through your bank or electronic transfer systems like NEFT, RTGS or IMPS, etc. Being ascertained about the working of this code will help you be aware of how you can use it to make quick and secure transactions.

If you are still confused regarding this code and want in-depth details related to it and other essential credentials, keep reading this guide to learn everything you need to know.

What is an IFSC Code?

Indian Financial System Code, abbreviated as the IFSC code, is a unique alphanumeric code of 11 digits. The sole purpose of the code is identification. Reserve Bank of India assigns an IFSC code to every branch of a bank present in India. You can find this code on your bank passbook and other documents as well.

This code enables RBI to monitor and keep track of the origination and final placement of your transactions. Your bank also uses this code to facilitate interbank communication throughout the time of transfer. It ensures security to the customer as well as speedy aids in times of any inconvenience.

Format for IFSC code

IFSC code is an 11 digit code and is in the format ‘WXYZ056789’. This code is segmented into three parts, each segment carrying some kind of information. These three segments are-

- The initial four digits represent the name of the bank

- The fifth digit is always a zero

- The last six digits indicate the branch code

This coded information is what helps the bank to understand the details behind a transaction.

Benefits of IFSC Code

Like mentioned earlier, the IFSC code is very crucial for transactions. Apart from being an identification code for your bank branch, it also has several other vital roles to play. Specific benefits of the code-

1) It helps one to make sure that payment reaches the intended account:

The IFSC helps to designate branches of a bank. Hence your payments reach their destination safely. Without this code, or even the misinterpretation of this code can lead to complications in your transaction.

2) Helps you to redeem instant payment services:

IFSC is required for all electronic transaction methods. These online services are quick and reliable, and IFSC plays a significant role in their successful completion.

3) Eliminates the chances of fraudulent activities:

As the IFSC helps the RBI and your bank to monitor your transactions minutely till it is completed. It acts as an added layer to your security; hence chances of fraud or fraudulent activities become close to none.

4) Makes online payments possible and straightforward:

You can sit anywhere and make payments with such ease that can be attributed to this unique code. It helps you to redeem and enjoy various services from the comfort of your homes.

How Does IFSC Code Work?

The IFSC provides information about the participating banks in a transaction. This unique code facilitates several electronic payment methods. The most frequently used online payment settlements like NEFT (National Electronic Funds Transfer) and RTGS (Real-Time Gross Settlement) are completed using this code.

The alphanumeric digits in this code contain information regarding the branches involved in the payment as well as the location of origin and ultimate destination. To complete the payment successfully, the bank requires the IFSC of the branches of both the remitter and beneficiary.

After the input of credentials, the IFSC code and other data provided by the remitter are recognized by the bank and recorded. The bank utilizes this information to carry out the entire process, and it is also used to take action in case of hindrance in the payment.

What happens when I put the wrong IFSC code?

While filling up details for a transfer, you have to ensure that you put the correct IFSC codes of both the branches involved along with the valid account credentials. It is crucial to ensure that you have entered the valid IFSC codes to ensure the transfer of funds to the desired bank account without any inconvenience.

If you input a wrong IFSC code, either the payment will not be completed successfully or will reach the wrong destination. Money credited into a wrong account cannot be procured back as transfers are usually not reversible.

Hence, here it becomes imperative to make sure that you have entered the correct details when you use both offline or online banking services. It makes sure that your payments reach the beneficiary account timely and safely. One has to be very careful while entering the bank credentials.

How to Find IFSC Code?

Your bank generally mentions the IFSC code of your branch in your bank documents. But there are several other ways to find it. Even though it might sound like a task, in reality, it is very easy to obtain it. Here are some ways to find your IFSC code-

Passbook and cheque book:

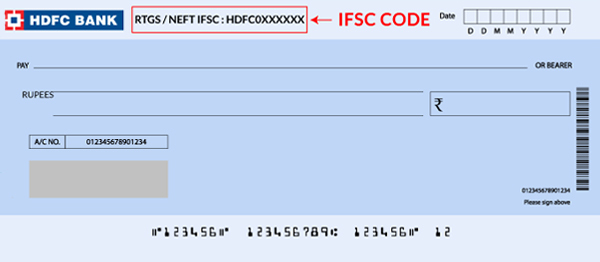

IFSC code is usually printed on your bank passbook. You can locate it on the first page of the passbook, along with the account number and other essential credentials. It can also be found on the cheque leaf.

RBI:

Your IFSC code can be obtained from the official website of RBI. It stores the bank credentials of every branch present in India.

Netbanking and Mobile banking:

You can find the code through the net banking or mobile banking portal of the bank. Just log in to the respected platform and look for your IFSC code.

Find Your Bank:

A very easy way to find your IFSC code is through the help of a website named ‘Find Your Bank.’ This website helps you find the IFSC and other important credentials of your bank account from the comfort of your home.

➔ Just go to their official website.

➔ Look for ‘Search IFSC code.’

➔ Enter all the required details in the drop-down options

➔ Select ‘Enter’

For example, if you need to find the IFSC code of the HDFC bank branch, select HDFC bank in the ‘Select Bank’ option, enter details regarding the name of your state, district, and the name of your branch and then click ‘Enter.’ You will be instantly provided with the IFSC code.

What makes it much more convenient is that they also have a mobile application, accessible anywhere anytime, making it very easy for you to find desired credentials in no time. Just in case all of these options do not work for you, then call the helpline number of your respective bank or branch.

What is MICR Code?

MICR code is also a unique code provided by your bank. It is utilized for reading, identifying, processing, and clearing your cheques. MICR or the Magnetic Ink Character Recognition technology is used to print the MICR code on the checkbook. This code is vital for successful cheque payments.

MICR Code Format

MICR code is a nine-digit code assigned by the RBI to every bank. The MICR code has three parts-

- The first three digits will give you the name of the city, which usually aligns with the PIN code used for postal addresses.

- Next three digits represent the name of the bank.

- The last three digits give the branch code.

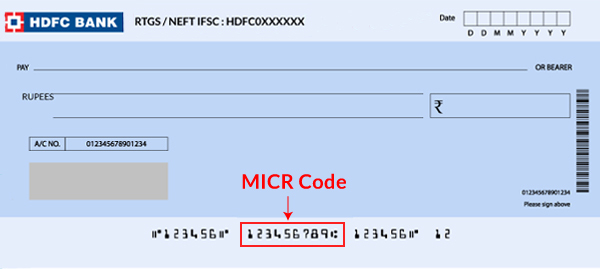

Where to locate MICR Code on Cheque book?

You can find your MICR codes easily on the checkbook of your bank account. It is printed on the bottom of the cheque leaf, next to the cheque number. Other ways to find the MICR code are:

Find Your Bank:

As mentioned earlier, Find Your Bank is the perfect place to obtain the MICR code. Visit their official website and enter the required details. Once you confirm, you will be provided with the credentials required.

RBI:

Visit the official website of RBI, and you can find your MICR code from their stored information.

Netbanking and mobile banking:

You can also obtain it from the online portals of your bank account. Just log into the portal with the necessary details. Contact the bank branch in case of any inconvenience.

Difference Between IFSC, MICR, SWIFT code

SWIFT code or the Society for Worldwide Interbank Financial Telecommunication code is a type of Bank Identifier Codes (BIC) and is another unique identification code your bank uses to complete fund transfers internationally. It plays a significant role in the authentication of your payment.

To understand further the significance of this code and how it differs from other codes like IFSC and MICR code read through the given table:

| IFSC code | MICR code | SWIFT code |

| It is used to complete interbank fund transfers across India, specifically electronic transactions. | This code helps in the processing and clearance of cheque payments. | It facilitates international fund transactions between two banks. |

| 11 digit alphanumeric code | 9 digit code | This code comprises 8-11 characters |

| ● The first four digits are representative of the bank ● fifth digit is a zero ● The last six digits indicate the branch of the bank | ● The first three digits represent the city, aligned with the PIN code. ● The following three digits represent the bank name. ● The last three digits here indicate the branch code. | ● The first four letters represent the bank. ● The next two letters depict the country where the bank is located ● The following two digits indicate the head office of the bank ● The last three digits indicate the branch |

| Issued by the RBI | Also issued by RBI | It is a code approved by ISO (International Organization for Standardisation) |

What is CIF Number?

CIF or the ‘Customer Identification File’ number is an electronic code comprising of 11 digits that contains all the personal data of the customers of a bank. It is also known as the Customer Information File. The loan, identity proof, KYC, and DEMAT details are all contained in this file for all accounts a consumer has with a bank.

The sole purpose of the CIF number is to hold all the necessary details of a customer for the different bank accounts they possess or the services utilized with the bank. It ensures the storage of these details in a safe place. The code is electronic and unique. It is provided for every customer for the respective bank account.

It makes all sorts of information accessible to the customer and also eliminates the occurrence of fraudulent activities. Hence it is an essential credential to be aware of.

You can find the CIF number from your bank documents like the passbook and chequebook on the first page. You can also go to the online banking portal and look for it in the account statement or summary. If you are still not able to find it, contact the customer care of your bank.

Methods Used for Money Transfer Using IFSC Code

With the emergence of digital transactions, making payments online is becoming very convenient for people. It is easy, time-saving as well as secure at the same time. Different payment methods are available to make hassle-free and quick payments throughout the country, but these are all done with the help of your IFSC code.

Some of the most popular options opted for are mentioned ahead:

NEFT or National Electronic Fund Transfer

NEFT, or the National Electronic Fund Transfer, is an electronic interbank transfer option initiated by the Reserve Bank of India to provide accessible online payment services to customers. This transaction works in settlements of batches, and it follows the Deferred Net Settling system or DNS system.

- Processed in batch settlements

- Charges can vary from Rs. 2.50 to Rs. 25 (GST applicable) depending on the amount of transaction. It could be different for different banks.

- Available all times.

- No minimum limit or maximum limit

Visit the online banking portals of your bank to redeem this service.

RTGS or Real-Time Gross Settlement

Real-Time Gross Settlement is another electronic payment service that settles transactions in real-time and in a gross system. These transfers are not reversible, and it usually opts for transactions of higher amounts.

- Processed on a real-time basis

- Charges can vary according to your bank

- Available in the banking hours.

- Minimum limit- Rs. 2 lakhs

- Maximum limit- No limit

You can make RTGS payments through online banking services provided by your bank.

IMPS or Immediate Payment Service

IMPS is an instant electronic fund transfer option, and it is available round the year at all times. To make a transaction through IMPS, use the internet or mobile banking service of your bank. To complete a successful IMPS transaction, you will require the following along with the IFSC code:

- MMID code

- Beneficiary’s MMID code

- Account number of beneficiary

- Your mobile number

- Beneficiary’s AADHAR number

Features of the IMPS method-

- Processed instantly

- Charges can vary according to the bank.

- Available all times.

- No minimum limit

- Maximum limit- Rs. 2 Lakhs

How to Register Beneficiary’s Account?

Registering the beneficiary is very important to ensure that the payment reaches the respected account safely. To successfully register a beneficiary, you will be required to provide-

- Beneficiary name

- Beneficiary account number

- Bank Name of Beneficiary

- Beneficiary address

- The limit of transfer

Steps to register a beneficiary:

- Log in to the net banking portal using your net banking credentials.

- Once you are safely logged in, go to the ‘Funds Transfer’ option, go to the ‘Request’ option, and select the ‘Add a Beneficiary.’

- Enter the required details mentioned above.

- After reviewing the details, click on confirm to complete the transaction.

Once you complete the registration, you can make transactions to the beneficiary using different payment methods.

Different Methods of Fund Transfer With the Help of IFSC Code

There are many ways to complete successful payments using the IFSC code. All the electronic payment services mentioned here can be redeemed in different ways. The process of making these payments is very convenient and easy. It requires very basic information.

Transfer through online platforms

You can easily make payments using the Netbanking portal of your bank and the mobile application. The steps are as explained below:

- Activate the net banking and mobile banking services through registration.

- Log into your account with the required credentials.

- Choose the type of fund transfer method ( Options would include- Between my accounts, Within Banks, IMPS, NEFT, via VISA, special visa payment).

- Enter required details of the beneficiary.

- Complete the transaction by entering the OTP (One Time Password), if required.

- Wait for the confirmation text. (In case of failure of payment, check if the amount is deducted from your account and raise a query immediately).

Using SMS Services

The SMS services on the phone can also be used to complete payments. It works in the following way:

- First, link your mobile number to the respective bank account through registration.

- To register, fill up the form in your branch, after which you will be provided with the starters kit with a unique 7 digit number called the MMID or mpin.

- Create an SMS by typing ‘IMPS’ along with the beneficiary’s necessary credentials, including their name, bank name, account number, IFSC code, and amount of remittance.

- Confirm the transaction, and you will receive a confirmation text wherein you will be required to fill in the mPin.

- After entering the mPin, click ‘ok,’ and you will complete your transaction.

You can pick one from the above-mentioned methods to enjoy several payment services available to you by using the IFSC code of your branch. These methods are very convenient and easy to complete. You just need to strictly follow the step-by-step guideline and keep convenient information ready.

FAQs

1) What is the full form of IFSC?

IFSC is an abbreviation for Indian Financial System Code. It is a unique 11 digit code assigned to every branch of a bank for their identification.

2) How to search for the bank name by IFSC code?

The first four letters in the IFSC code indicate the name of your bank. You just need to look for these characters and use them to find your bank’s name easily. For example, if the IFSC code is ICIC0001234, the initial four letters tell you that it is the ICICI bank.

3) What is RTGS and NEFT Code?

The IFSC code is often referred to as the RTGS and NEFT code because the IFSC code is vital to complete the payments made through these services. Hence the IFSC code is often confused with the NEFT or RTGS code.

4) Is Branch Code and IFSC code the same?

No, the Branch code and the IFSC code are not the same. Branch code is indicative of a specific branch, and it is encoded within the last six digits of the IFSC code. IFSC indicates the bank and its branch, and the Branch code is a part of it.

5) Are SWIFT and IFSC codes the same?

IFSC and SWIFT codes are different. IFSC code is the ‘Indian Financial System Code,’ which is used to provide unique identification to a bank branch.

Whereas the SWIFT code stands for ‘Society for Worldwide Interbank Financial Telecommunication,’ which is used to complete fund transfers internationally, and it also helps in identifying the bank but not the branch. They completely differ in their functionality.

6) Can I find my IFSC code by account number?

Your bank account number does not contain the IFSC code, but you can use the account number to find out the IFSC code. All the procedures mentioned in the article to find the IFSC code require the bank account number.

7) Can I Get the IFSC code from my bank passbook?

Yes, you can find the IFSC code in the passbook. It is present on the first page of your bank passbook along with other bank account credentials. It is an 11 digit alphanumeric code in the format’ WXYZ01234.’

Leave a Reply